SEC Rule Amendments and Dual-class returns

Yvan Allaire and François Dauphin | Commentary #11. ISS is finally leashed: SEC Amends Rules for Proxy Advisors

On July 22, 2020, the Securities and Exchange Commission (SEC) adopted amendments to better regulate the activities of proxy advisors, such as ISS and Glass Lewis, and to ensure that clients of proxy voting advice businesses have reasonable and timely access to more transparent, accurate and complete information on which to make voting decisions.

In essence, proxy advisors have always benefited from an exemption from the information, legal risks and filing requirements of proxy solicitation. The SEC has now stipulated that this exemption will apply in the future only if proxy advisors abide by the following conditions:

- They must provide specified conflicts of interest disclosure in their proxy voting advice or in an electronic medium used to deliver the proxy voting advice;

- They must have adopted and publicly disclosed written policies and procedures reasonably designed to ensure that corporations that are the subject of proxy voting advice have such advice made available to them at or prior to the time when such advice is disseminated by the proxy advisors to their clients;

- They ensure their clients will receive, in a timely manner, any statement, explanation and contestation issued by the corporations that are the object of the voting recommendation.

The SEC is thus responding to oft-stated concerns of many issuers about these heretofore lightly regulated but influential market participants.

Proxy advisory firms are not required to comply with the amended regulations until December 1, 2021.

Of course, ISS has already announced its intention to challenge in court this SEC ruling.

IGOPP is particularly pleased with the SEC’s amended regulations as it called for such actions in a 2013 Policy Paper, The Troubling Case of Proxy Advisors: Some policy recommendations.

The complete press release of the SEC, and the links to retrieve pertinent materials, can be accessed here.

2. New study on relative performance of US dual-class companies

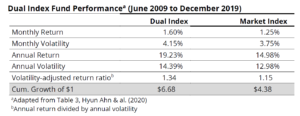

In a novel approach to the subject, researchers have “constructed” an index of dual class shares for the period 2009-2019. The intention here is to assess the performance of a hypothetical fund that would be made up of all dual class shares in proportion to their stock market capitalization. The performance of the fund may then be compared to other index funds, such as, in this case, the CRSP US Total Market Index. The results for dual class voting structures speak for themselves, as shown in the Table below.

Clearly, the volatility-adjusted return ratio of the Dual Index (a close variant of the Sharpe ratio where the higher the ratio the better) is clearly superior to the ratio of the Market Index.

The Index includes all dual-class companies with ordinary common shares listed on NYSE, NASDAQ, or AMEX and total market capitalization in excess of $100 million. A reconstitution process of the Dual Index is carried out semiannually, at the end of June and December. In case of a delisting or collapse of the dual-class structure, the researchers reinvested the proceeds in the portfolio until the next Dual Index reconstitution.

As of December of 2019, the Dual Index included 178 dual-class companies valued at $3.4 trillion. The Index accounts for 89% of the market capitalization of all dual-class companies listed across major U.S. stock exchanges.

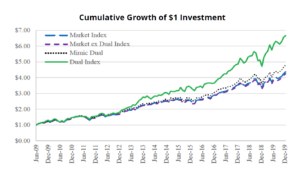

The next figure shows the cumulative growth of a one-dollar investment in the Dual Index (green line) relative to the cumulative growth of a one-dollar investment in the market index (blue line). The performance of the Dual Index is especially strong in the second half of the decade .

The complete study by authors Byung Hyun Ahn, Jill E. Fisch, Panos N. Patatoukas & Steven Davidoff Solomon, released as Research Paper on July 28, 2020, is available here.